Comment on Simon Wren-Lewis on ‘The NAIRU: a response to critics’ and Lars Syll on ‘Simon Wren-Lewis — flimflam defender of economic orthodoxy’

Blog-Reference and

Blog-Reference and

Blog-Reference and

Blog-Reference on Mar 4

The NAIRU-Phillips Curve is an explicit formal description of the functioning of the macroeconomic labor market. Formal description means that one has a number of variables and their relationships which summarize the current knowledge of how the economy or some part of it works.

Scientific knowledge is embodied in the true theory.

Right policy depends on true theory: “In order to tell the politicians and practitioners something about causes and best means, the economist needs the true theory or else he has not much more to offer than educated common sense or his personal opinion.” (Stigum)

The two questions that arise with any description are: (i) is it conceptually/logically consistent, and (ii), is it materially consistent? The second question involves the measurability of variables, the practical problem of measurement, data gathering, and statistical methodology. From a description that is either formally inconsistent or materially inconsistent ANY economic policy conclusions can be drawn. Put the other way round, policy proposals that are not based on a materially/formally consistent theory are at the same level as sitcom blather, storytelling, or soapbox agenda pushing.

Economic policy guidance that is not based on the true theory is pretty much the same as ancient Roman poultry entrails reading.

The NAIRU-Phillips Curve is scientifically worthless because it is conceptually inconsistent.#1 So, any discussion about measurement problems or the economic policy implications of a NAIRU is pointless. Needless to emphasize that most of the discussion circles around these distracting side issues.

The NAIRU-Phillips Curve is an integral part of standard economics: “The concept of the NAIRU, or equivalently the Phillips Curve, is very basic to macroeconomics. It is hard to teach about inflation, unemployment and demand management without it.”#2

Standard economics is built upon this set of foundational propositions, a.k.a. axioms: “HC1 economic agents have preferences over outcomes; HC2 agents individually optimize subject to constraints; HC3 agent choice is manifest in interrelated markets; HC4 agents have full relevant knowledge; HC5 observable outcomes are coordinated, and must be discussed with reference to equilibrium states.” (Weintraub)

It should be pretty obvious that the standard axiom set contains THREE NONENTITIES: (i) constrained optimization HC2, (ii) rational expectations HC4, and (iii) equilibrium HC5.

Methodologically, the neo-Walrasian axioms are forever unacceptable but scientifically incompetent economists from Jevons/Walras/Menger onward accepted them as defining the ‘language of economics’: “Accepting the concept of the NAIRU does not mean you have to agree with their judgments. But if you want to argue that they could be doing something better, you need to use the language of macroeconomics.”#2

Not at all! The neo-Walrasian language of macroeconomics is composed of NONENTITIES and this leads quite naturally to measurement problems, material inconsistency, and vacuous political blather. So Heterodoxy is right in saying that “the NAIRU has to be bashed, smashed, and trashed”.

The problem of traditional Heterodoxy is that it has nothing better to offer.#3 The standard microfoundations HC1/HC5 are false, but Keynesian macrofoundations are also false. So, both orthodox and traditional heterodox labor market theories are proto-scientific rubbish.#4 As an inevitable consequence, the whole discussion about NAIRU has degenerated to the squabble of political sects. Wren-Lewis tries in vain to deny this plain fact: “Economics is certainly not a religion, where all you have to do is choose which sect you belong to and then follow great works.“

What has to be done to get out of confused sectarian squabble is to fix the labor market theory by putting it on consistent macrofoundations.

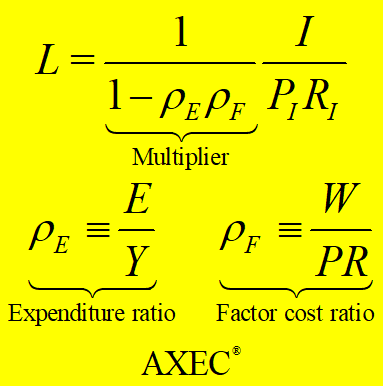

Two factors determine macroeconomic employment: overall demand and the price mechanism, or more specifically, the actual configuration of average wage rate, price, and productivity. As a consequence, economic policy is about private/public demand management AND wage/price management.

The correct theory of the macroeconomic price mechanism tells us that ― for purely SYSTEMIC reasons ―

the average wage rate has in the current situation to rise faster than the average price. THIS opens the way out of mass unemployment, deflation, and stagnation and NOT the blather of scientifically incompetent orthodox and heterodox agenda pushers.#4

Egmont Kakarot-Handtke

#1

NAIRU, wage-led growth, and Samuelson’s Dyscalculia

#2 See SWL ‘

The NAIRU: a response to critics’

#3 See LPS ‘

Simon Wren-Lewis — flimflam defender of economic orthodoxy’

#4

Mass unemployment: The joint failure of orthodox and heterodox economics

Related '

Why is economics a total scientific failure?'. For details of the big picture see cross-references

Employment/Phillips Curve.

Legend: employment L, Wage rate W, price P, productivity R, expenditures E, income Y

***

The fatal mistake of the discussion is to accept the NAIRU-Phillips Curve (with the well-known disclaimers) and to focus on the economic policy implications with regard to the given situation in the US/UK/etc. But there is NO use to discuss policy if the underlying theory is defective.

The fact of the matter is that the Phillips Curve is misspecified since Samuelson/Solow.#1 Because there is NO such thing as a NAIRU-Phillips Curve all political discussion is vacuous.

***

to Tom Hickey on Feb 28

You say: “The relationship between employment and inflation appears to be contingent and based on a number of factors, including institutional factors, that result in dynamic conditions involving uncertainty.”

This is an entirely vacuous econ-waffle. Imagine, as a contrast, a physics teacher tells his students about gravitation: “The relationship between velocity and mass appears to be contingent and based on a number of factors, including history-specific factors, that result in dynamic conditions involving uncertainty.”

It is pretty obvious that economists have NOTHING of substance to say. Why do they not simply shut up?

The elementary dependency between employment and inflation and a number of other factors is given with this

objective systemic equation that is composed of MEASURABLE variables.

This equation is the economic equivalent to Galileo’s Law of Fall and thus the ultimate econ-waffle stopper.

***

REPLY to Auburn Parks on Feb 28

You say: “There is a simple reason why physics like precision and predictability is inapplicable to economics, and its because of the reasons Tom provided.”

The simple reason is scientific incompetence. For details see

Failed economics: The losers’ long list of lame excuses.

***

REPLY to Ralph Musgrave on Feb 28

You say: “You make the naïve mistake many people make of thinking the because something cannot be measured accurately that therefore it does not have a precise value.”

You make the same mistake as all illiterate persons, that is, you cannot read. What I have clearly stated is: “NAIRU is dead, not because of measurement problems, but because the underlying employment theory is false.”#1 The measurement problem is a side issue.#2

#1

NAIRU: an exhaustive dancing-angels-on-a-pinpoint blather

#2

NAIRU and the scientific incompetence of Orthodoxy and Heterodoxy

***

REPLY to Auburn Parks on Feb 28

The moronic part of economists, i.e. the vast majority, maintains that economics is a social science. Time to wake up to the fact that economics is a systems science.#1

Economics is NOT a science of individual/social/political behavior — this is the social science delusion — but of the behavior of the monetary economy. All Human-Nature issues are the subject matter of other disciplines (psychology, sociology, anthropology, biology/ Darwinism, political science, social philosophy, history, etcetera) and are taken in from these by way of multi-disciplinary cooperation.#2

The economic system is subject to precise and measurable systemic laws.#3

#1

Lawson’s fundamental methodological error and the failure of Heterodoxy

#2

Economics and the social science delusion

#3

The three fundamental economic laws

***

REPLY to Noah Way on Mar 1

You say: “’Economic science’ is an oxymoron.”

It is, first of all, of utmost importance to distinguish between political and theoretical economics. The main differences are: (i) The goal of political economics is to successfully push an agenda, the goal of theoretical economics is to successfully explain how the actual economy works. (ii) In political economics anything goes; in theoretical economics, the scientific standards of material and formal consistency are observed.

Political economics has produced NOTHING of scientific value in the last 200+ years. The four major approaches — Walrasianism, Keynesianism, Marxianism, Austrianism — are mutually contradictory, axiomatically false, and materially/formally inconsistent.

A closer look at the history of economic thought shows that theoretical economics (= science) had been hijacked from the very beginning by the agenda pushers of political economics. These folks never rose above the level of vacuous econ-waffle. The whole discussion from Samuelson/Solow’s unemployment-inflation trade-off to Friedman/Phelps’s natural rate to the rational expectation NAIRU is a case in point.

The NAIRU-Phillips Curve has zero scientific content. It is a plaything of retarded political economists. Samuelson, Solow, Friedman, Phelps, and the rest of the participants in the NAIRU discussion up to Wren-Lewis are fake scientists.#1

#1

Modern macro moronism

***

REPLY to Ralph Musgrave on Mar 1

It would be fine if you could first learn to read and to think and to do your economics homework.

The point at issue is the labor market theory and the remarkable fact of the matter is that economists have after 200+ years NO valid labor market theory. The proof is in the NAIRU-Phillips Curve. So what these failures are in effect doing is giving policy advice without sound theoretical foundations. Scientists don’t do this.

What is known since the founding fathers about the separation of politics and science is this “A scientific observer or reasoner, merely as such, is not an adviser for practice. His part is only to show that certain consequences follow from certain causes, and that to obtain certain ends, certain means are the most effectual. Whether the ends themselves are such as ought to be pursued, and if so, in what cases and to how great a length, it is no part of his business as a cultivator of science to decide, and science alone will never qualify him for the decision.” (J. S. Mill)

The first point is that economists violate the separation of politics and science on a daily basis.#1 The second point is that their unwarranted advice is utter rubbish because they have NO idea how the economy works. The problem society has with economists is that it would be much better off without these clowns.

You ask me: “Why then don’t you advocate a massive increase in demand. Think of the economic benefits and social problems solved.!!”

Answer: The business of the economist is the true theory about how the economic system works and NOT the solution to social problems. This is the proper business of politicians. In addition, an economist who understands how the price and profit mechanism works does not make such a silly proposal, only brain-dead political agenda pushers do.#2

What I am indeed advocating is that retarded econ-wafflers are thrown out of economics and that economics gets finally out of what Feynman aptly called cargo cult science.#3

Economists claim for more than 200 years that they are doing science and this is celebrated each year with the ‘Bank of Sweden Prize in Economic Sciences in Memory of Alfred Nobel’. Time to make this claim come true.

The only thing economist like you can actively do to contribute to the progress of economics is switching on the TV and watching 24/365.

#1

Scientific suicide in the revolving door

#2

Rethinking deficit spending

#3

Economists and the destructive power of stupidity

***

REPLY to Ralph Musgrave on Mar 1

You say: “Ergo economics have a duty to give the best advice they can in the circumstances.”

The only duty of scientifically incompetent economists is to throw themselves under the bus. Economists are a menace to their fellow citizens as Napoleon already knew: “Late in life, moreover, he claimed that he had always believed that if an empire were made of granite the ideas of economists if listened to, would suffice to reduce it to dust.” (Viner)

Economists do NOT solve social problems they ARE a social problem.

You repeat your silly question: “So why are you so reluctant to solve those social problems by advocating a huge increase in demand. It’s blindingly obvious.”

Yes, it is blindingly obvious that deficit spending does NOT solve social problems but CREATES the social problem of an insanely unequal distribution (see the references above).

This follows from the true labor market theory which is given with the systemic Employment Law.#1 “The correct theory of the macroeconomic price mechanism tells us that ― for purely SYSTEMIC reasons ― the average wage rate has in the current situation to rise faster than the average price. THIS opens the way out of mass unemployment, deflation, and stagnation and NOT the blather of scientifically incompetent orthodox and heterodox agenda pushers.”#2

Right policy depends on true theory: “In order to tell the politicians and practitioners something about causes and best means, the economist needs the true theory or else he has not much more to offer than educated common sense or his personal opinion.” (Stigum)

Economists do not have the true theory. They have NOTHING to offer. The NAIRU-Phillips Curve is provably false. Because of this ALL economic policy conclusions drawn from it are counterproductive, that is, they WORSEN the situation. So, Samuelson, Solow, Friedman, Phelps, and the other NAIRU-Phillips Curve proponents bear the responsibility for mass unemployment and the social devastation that comes with it.

From the fact that the NAIRU labor market theory is false follows that economists are incompetent scientists and that ALL their economic policy proposals are scientifically worthless.

#1

NAIRU: an exhaustive dancing-angels-on-a-pinpoint blather

#2

NAIRU and the scientific incompetence of Orthodoxy and Heterodoxy

***

REPLY to Anonymous on Mar 05

For the final word on NAIRU see the comment on David Glasner’s recycling of dead but not yet buried Phillips Curve stuff

NAIRU and economists’ lethal swampiness.

You are certainly right in stressing that economics is not a religion: actually, it is fake science. This applies to Walrasianism, Keynesianism, Marxianism, and Austrianism.

Related '

NAIRU: an exhaustive dancing-angels-on-a-pinpoint blather' and '

NAIRU does not exist because equilibrium does not exist' and '

If it isn’t macro-axiomatized, it isn’t economics'

{kind=link}